Overview

PaySprint is launching cash management services API to their API Partner network from various domains such as e-commerce, micro-finance, commercial vehicle financing, two-wheeler financing, auto financing, logistics, insurance companies, telecom. As part of this service, its API Partners are utilized for the purpose of cash burial either by the employees of the client or directly by the customers of the client. For the customers and agents, this facility provides a new avenue for cash payments in their local neighbourhood, saving time and effort. For the client, this service helps to reduce cash in their ecosystem and minimizes cash risk enabling them to focus on their core business. A majority of players who digital products or sell products digitally don’t have a way to reach customers who deal in cash or are unable to pay using digital methods. This is where PaySprint comes in to help such organizations to accept payments of EMIs/collection in cash.

Goals

Balancing cost, cash-flow and risk

Potential Benefits:

- Ease in managing cash for the clients in the market.

- Flexibility to the customers/agent to dump cash anywhere at any time.

- Instant conversion and low risk of cash handling.

Specifications

We are opening our API network to allow other organizations to accept cash payments as a cash deposition centre which is the major problem statement these days for the clients to get the EMI/Premium collected in cash specially for those who earn in cash. We at PaySprint work majorly with the type API Partners who deal with customers who earn in cash and whosoever would want to pay EMI/insurance premium/drop cash at any of their (API Partner’s) merchant outlets.

PaySprint will be exposing their open banking cash drop service API to their API Network so that they can facilitate Airtel Payments Bank Limited (APBL) for collection of cash, EMI and loan payments on our Client’s (like Zomato , Bajaj Finance etc.) behalf, embedded at the back end.

API Partner’s merchant and distributor outlet/points are expected to act as cash burial points and any client’s such as Zomato/Bajaj Finance etc. agent/customer can walk-in and deposit cash against their company with their unique ID i.e.. Loan ID or mobile no. or EMI ID or policy ID etc.

Services available in cash drop module: -

- Cash drop

- Loan payment

- Policy payment

- EMI payment

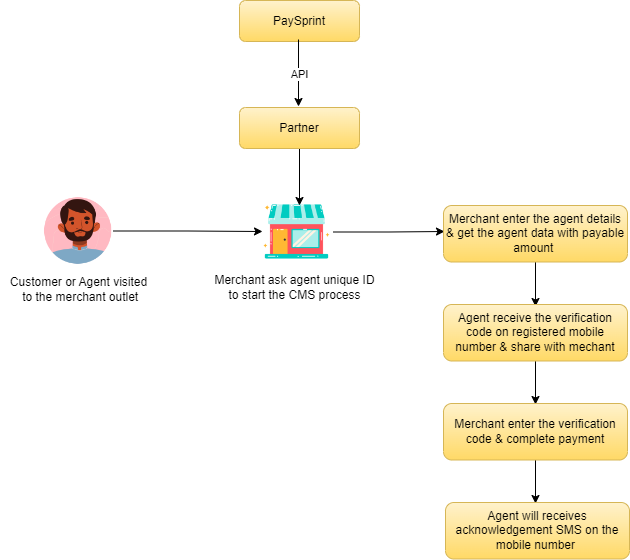

- The client’s representative/customer shall visit the authorized API's merchant and distributor outlet/points with the cash in hand during business hours from 9:30 A.M to 6:30 P.M (Monday to Friday plus odd Saturdays) depending on their partners, except on designated holidays and Sundays.

- The API Partner’s merchant and distributor whitelisted outlet/points shall log into their portal and ask for the name of the client’s representative and check his office ID or PAN ID to avoid fraudulent cases.

- The nominated agent of API Partner's Outlet shall initiate the cash collection by requesting the mobile number of the client’s representative along with the cash drop amount.

- Client’s representative/Customer walk-in shall share the authentication code received on his/her registered mobile number to initiate the transaction.

- Depositor’s mobile no. needs to be taken and it should also be OTP verified by the Partner itself to ensure depositor communication and a smooth refund (in minimal no. of cases).

- Confirmation screen or pop up before the payment should be implemented in the product flow to avoid escalations later.

- API Partner’s merchant will enter the required input fields (such as policy ID / EMI ID /loan ID, name of the biller) on behalf of the customer representative and proceed with the transaction.

- API Partner shall provide digital receipt of cash deposit via SMS confirmation of complete or successful transaction to the depositor/ the Client’s representative on the mobile no. shared earlier.

- PaySprint will also share the enquiry API with API Partner network, so that we can check the status of the timed-out cases.

- Also, on the retailer’s portal a success screen must be implemented.

- After a successful or Failed transaction, merchant can’t initiate a new CMS transaction on the same URL.

- If Merchant initiate a new transaction on the successful or failed transaction URL & wallet get debited then PaySprint will won’t the liable.

- Any addition of billers / CMS partners at the credit side, an NFA is supposed to be raised by the bank and approved with finance first till the time it’s made automatic.

- After successful CMS transactions merchant need to cut the redirected page so that merchant comeback to home page.

Process flow